There’s a detail buried inside the Urban Institute’s latest analysis of the One Big Beautiful Bill Act that deserves far more attention than it’s gotten.

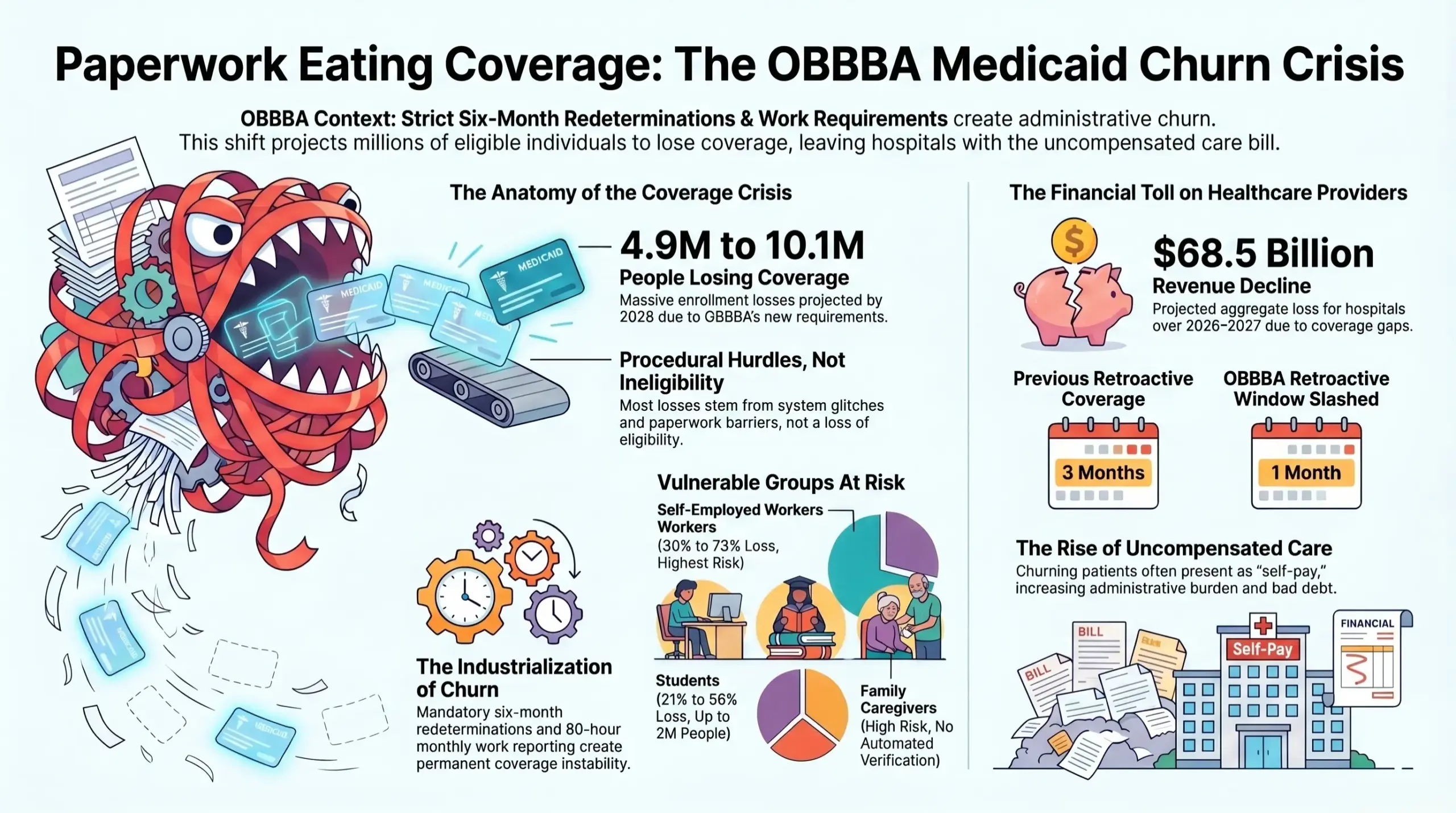

Researchers modeled how many people will lose Medicaid under OBBBA’s new work requirements and six-month redeterminations, effective January 1, 2027. Their projections range from 4.9 million to 10.1 million people losing coverage by 2028. But here’s the part that matters for anyone who works in a hospital: a significant share of those people will be fully eligible for Medicaid. They won’t lose coverage because they stopped working. They’ll lose it because a data system couldn’t confirm they were working, or because they didn’t know they had to submit paperwork, or because the form didn’t arrive, or because the state’s eligibility infrastructure simply wasn’t built for this volume.

The Urban Institute called it directly — the risk of losing Medicaid is “not primarily a function of whether someone qualifies, but whether a state’s data systems can confirm it automatically.”

That distinction matters enormously. It means the coming wave of Medicaid disenrollments isn’t mostly a story about people losing eligibility. It’s a story about paperwork eating coverage — and hospitals will absorb the financial consequences of every single gap.

We’ve Watched This Movie Before

This isn’t a hypothetical scenario. It already happened.

When pandemic-era continuous enrollment protections ended and states began redetermining Medicaid eligibility in 2022, more than 25 million people were disenrolled from Medicaid over the following two years. Analysts who reviewed the data found that a substantial portion of those disenrollments were procedural — people removed not because they were ineligible, but because they missed a notice, couldn’t complete an online-only renewal, or fell through the cracks of an overwhelmed state eligibility system. Many of them were re-enrolled shortly after, confirming they had been eligible the whole time.

Now imagine that process running twice a year, every year, permanently — which is exactly what OBBBA’s six-month redetermination requirement creates.

And layered on top of that: work requirements demanding that non-disabled adults ages 19–64 document 80 hours per month of qualifying activity. When Georgia piloted its Pathways to Coverage program with work requirements, fewer than 7,500 people enrolled out of an estimated 300,000 potentially eligible adults — not because they didn’t meet the requirement, but because of confusing reporting processes, online-only documentation, and the simple reality that navigating government paperwork is hard when you’re working inconsistent hours, moving between jobs, or caring for a family member.

In Arkansas and Georgia, the two states where full implementation of work requirements occurred, members experienced significant access barriers due to system glitches, unclear reporting processes, and limited support options. Staff and training needed to support implementation were consistently underestimated, resulting in service delays and increased burden on frontline workers.

OBBBA is now requiring every expansion state to replicate that experience — on a far larger scale, with a compressed implementation timeline.

The Five Patients Most Likely to Fall Through

The AJMC recently detailed which Medicaid enrollees face the highest procedural disenrollment risk under OBBBA. The pattern is consistent: these are people who are eligible, but who face verification systems that can’t automatically confirm it.

Caregivers caring for disabled family members are explicitly exempt from work requirements — but automatic verification of caregiving status is nearly impossible with existing state data systems. Without automated confirmation, they’ll be required to manually document their status. Based on prior state experience, a substantial share won’t successfully navigate that process.

Students enrolled at least half-time are also compliant — but part-time enrollment status isn’t consistently collected on Medicaid applications, and most states haven’t yet integrated student data systems like the National Student Clearinghouse into eligibility workflows. Under the low mitigation scenario, states are assumed to be unable to automatically identify students at all, requiring manual verification — with projected enrollment losses for students ranging from 21% to 56%, affecting as many as 2 million people.

Self-employed individuals — gig workers, freelancers, sole proprietors — face the highest projected losses of any subgroup, ranging from 30% to 73%, because their income and work hours are difficult to verify through traditional wage reporting systems.

People with chronic conditions who may qualify for medical frailty exemptions will depend on how their state defines “frailty” — a term OBBBA left deliberately vague, with significant variation expected in how states operationalize it.

Patients near the income thresholds who fluctuate above or below eligibility limits between redetermination cycles will cycle in and out of coverage constantly — the exact definition of Medicaid churn.

What Churn Costs a Hospital

Medicaid churn — the cycle of losing and regaining coverage — has always existed. OBBBA industrializes it.

For revenue cycle teams, a churning patient is one of the most expensive accounts to manage. The patient may present while technically uninsured (between a disenrollment and reenrollment), which misclassifies the account as self-pay. If eligibility is retroactively restored, the window to refile has already shrunk — OBBBA cuts retroactive Medicaid coverage for expansion enrollees from three months to just one. That means the margin for error on retroactive billing recovery just got dramatically tighter.

External reporting estimates hospital net revenue declines totaling $68.5 billion over 2026–2027, with more than $12 billion in additional uncompensated care, and many systems facing net patient revenue contractions between 2% and 10%. That’s the aggregate financial story. The operational story is told at the account level — in misclassified self-pay patients, in missed retroactive filing windows, in enrollment applications that started but never finished because a patient didn’t understand the next step.

The Hospital’s Role Has Changed

Hospitals have historically treated Medicaid enrollment as a social work function — something that happens in a back office or through a financial counselor who catches patients at discharge. That model wasn’t built for an environment where coverage is structurally unstable, redeterminations are twice-annual, and the difference between a billable account and uncompensated care is whether someone found the right form in time.

The hospitals managing this well aren’t waiting for patients to show up uninsured and then scrambling to enroll them. They’re building enrollment support into patient touchpoints that happen before, during, and after care — treating coverage as a continuous process rather than a front-end checkbox.

That’s a fundamentally different way of thinking about the relationship between a hospital and its uninsured or at-risk patients. It’s also, increasingly, an operational necessity.

RevOne has been doing this work since 2003 — helping revenue cycle teams identify coverage gaps and guide patients through ACA Marketplace, Medicare, and Medicaid enrollment before accounts age into bad debt. In an environment where the structural drivers of coverage loss are accelerating, that kind of proactive, community-based enrollment support isn’t a supplemental program. It’s core infrastructure.

The Quiet Irony of OBBBA

Here’s what makes the OBBBA coverage story particularly hard to absorb: most of the people who will lose Medicaid next year won’t lose it because they stopped being poor, stopped working, or stopped needing healthcare. They’ll lose it because a state system couldn’t automatically confirm something that was true.

That’s not a political judgment — it’s an operational one. And for hospitals, the question isn’t whether to have an opinion about the policy. It’s whether your enrollment and eligibility infrastructure is built to catch the people who fall through its gaps.

Because they will show up in your ED. They will be in your clinics. They will be scheduled for procedures. And whether they arrive as covered patients or uncompensated care will depend, in many cases, on whether someone helped them navigate the paperwork before coverage lapsed.

That window — between when a patient starts losing coverage and when the account becomes a write-off — is exactly where RevOne works.