Ask any hospital CFO what’s driving the revenue pressure this year, and you’ll hear variations of the same answer: ACA enrollment dropped, premiums spiked, uninsured volumes are up. All true. All well-documented.

But there’s a quieter version of the same problem sitting inside accounts your system currently shows as active and covered — patients who are still technically enrolled in Marketplace plans, still showing up as insured in your eligibility checks, but whose coverage is already on a countdown clock your revenue cycle team may not be watching.

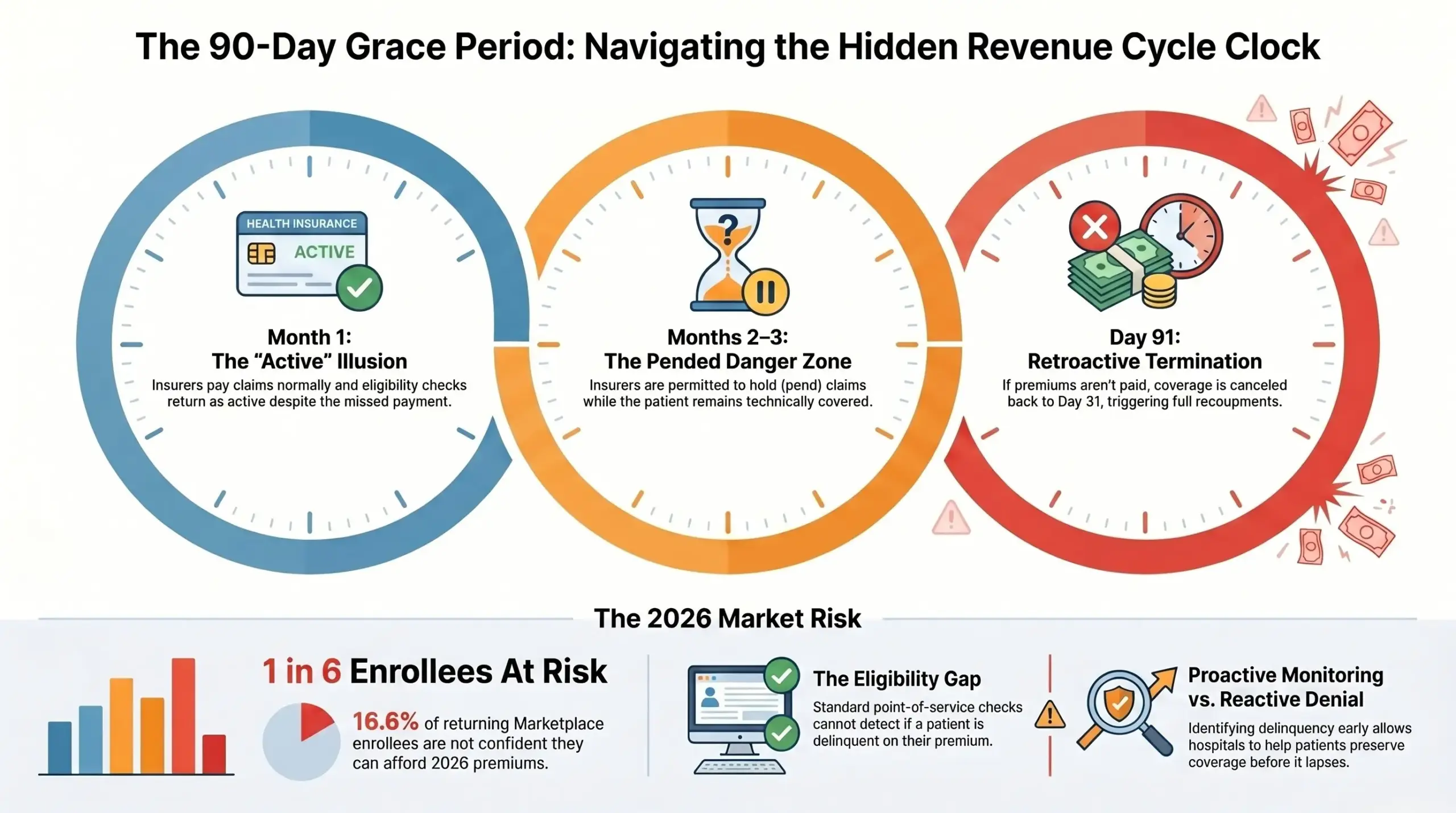

It’s called the 90-day grace period. And in 2026, with a KFF survey finding that 1 in 6 returning Marketplace enrollees say they’re not confident they can afford their monthly premiums through the end of the year, it has become one of the most underappreciated recoupment risks in healthcare revenue cycle management.

How the Clock Works

Under ACA rules, a subsidized Marketplace enrollee who misses a premium payment doesn’t immediately lose coverage. They get a 90-day grace period — three months to catch up before the insurer can terminate coverage retroactively back to day 31.

Here’s how that plays out in practice for a hospital:

In month one of the grace period, the insurer pays claims normally. The patient appears active. Nothing in your eligibility verification flags a problem.

In months two and three, the insurer is permitted to pend claims — hold them without paying — while the patient remains technically covered. If the patient never pays the overdue premium, the insurer terminates coverage retroactively to the end of month one. Claims for services in months two and three may be pended, denied, or subject to recoupment depending on how they were processed and applicable state rules. The hospital is left billing a patient who was never going to pay a premium, for services that will never be reimbursed.

That’s not a hypothetical edge case. It’s the structural design of the grace period, and it becomes a volume problem the moment a meaningful percentage of your Marketplace patients are financially stretched — which, in 2026, is exactly the situation.

The Scale of the Exposure Right Now

Consider the numbers from the current environment. About 4% of returning Marketplace enrollees said they had not yet paid their first premium for 2026. For enrollees receiving advance premium tax credits, a three-month grace period generally applies after at least one month of coverage has been effectuated, meaning timing can vary based on when coverage began and when payments became delinquent.

That survey was conducted in late March. The grace period cascades forward throughout the year for every month a payment is missed.

One in six returning Marketplace enrollees say they are not confident they will be able to afford their monthly health insurance premium for the entirety of 2026. That’s not a small fringe — it’s a statistically significant share of your Marketplace payer mix. And a majority of returning enrollees say they are cutting back spending on food or basic household items in order to afford the costs of coverage and care.

When patients are choosing between groceries and insurance, some will stop paying premiums. The 90-day window means hospitals won’t see the financial consequence of that decision immediately. They’ll see it 60 to 90 days later — in recoupments, in pended claims, in accounts that looked clean on the date of service and look very different two months later.

HCA Healthcare’s CFO noted that the figure for uninsured equivalent admissions includes their best estimate of attrition from patients who initially enrolled for 2026 but dropped coverage by failing to pay their monthly premium following expiration of enhanced subsidies. If a system the size of HCA is modeling this as a material category, revenue cycle teams at every hospital should be treating it the same way.

Why Eligibility Checks at the Point of Service Aren’t Enough

The standard defense against grace period exposure is eligibility verification — checking coverage before every encounter. It’s good practice, and it’s necessary. But it doesn’t solve the grace period problem, because the problem is invisible at the point of service.

During month one of the grace period, a patient’s eligibility returns active. Claims process normally. Nothing triggers a review. It’s months two and three — after you’ve provided care and filed claims — where the risk is hiding.

One of the most direct ways to actively manage grace-period exposure is to identify which Marketplace patients are currently delinquent on premium – before you’re notified of a recoupment. That requires monitoring, not just point-in-time verification.

Plan selection data does not accurately reflect the number of people who ultimately have ACA Marketplace coverage because it does not account for premium payments — it shows how many people have selected a plan, but not how many are actually maintaining coverage. The same gap exists inside your revenue cycle: an active eligibility status doesn’t tell you whether the premium behind that plan is actually being paid.

Two Different Risks, One Shared Solution

The grace period is sometimes framed purely as a recoupment risk — a defensive concern about getting paid back for work already done. That framing is incomplete.

The more valuable lens is this: a patient in the grace period is a patient whose coverage is salvageable. They haven’t lost insurance yet. If someone reaches them, explains the consequence of non-payment, helps them understand their options — whether that’s catching up on premiums, exploring a different plan at lower cost, or evaluating whether they now qualify for Medicaid given an income change — coverage may be preserved or restored. The hospital has a better chance of securing reimbursement, and the patient has a better chance of staying insured.

That’s the logic behind RevOne’s Delinquent Premium Monitoring service. Rather than waiting for recoupments to arrive and then trying to recover, the intervention happens inside the grace period window — identifying delinquent Marketplace patients, engaging them before coverage lapses, and resolving the delinquency before it becomes a denied claim or a write-off.

In an ordinary year, this is good revenue cycle hygiene. In 2026, with average Marketplace premiums rising significantly in 2026 and a meaningful share of Marketplace enrollees already signaling they’re struggling to pay, it’s become a front-line financial protection.

The Bigger Pattern

What the grace period issue illustrates is something broader about where healthcare revenue cycle management is heading.

For years, the dominant RCM model has been reactive: verify eligibility at intake, file claims, manage denials, pursue collections. That model was built for a relatively stable insurance environment where a patient who was covered at the point of service stayed covered when the claim processed.

That stability is eroding. Policies that have defined the coverage landscape for the past four years are gone. Premiums are at their highest in nearly a decade. Medicaid churning is about to accelerate dramatically. Grace periods are filling with patients who enrolled in January and are now struggling to pay May.

The revenue cycle teams adapting to this environment share a common trait: they’ve moved their coverage intervention earlier. They’re not just verifying coverage — they’re monitoring it. Not just enrolling patients once — but staying in contact through the financial lifecycle that determines whether coverage stays active.

That’s a different kind of partnership than a billing vendor or a collections agency provides. It’s the kind RevOne has been building with hospital revenue cycle teams for over two decades.

Because in a year when your “covered” patients need more than a coverage check, the question is who’s watching the clock with you.