For years, expanded ACA premium tax credits kept millions of patients covered and hospital uncompensated care costs in check. That era ended on December 31, 2025.

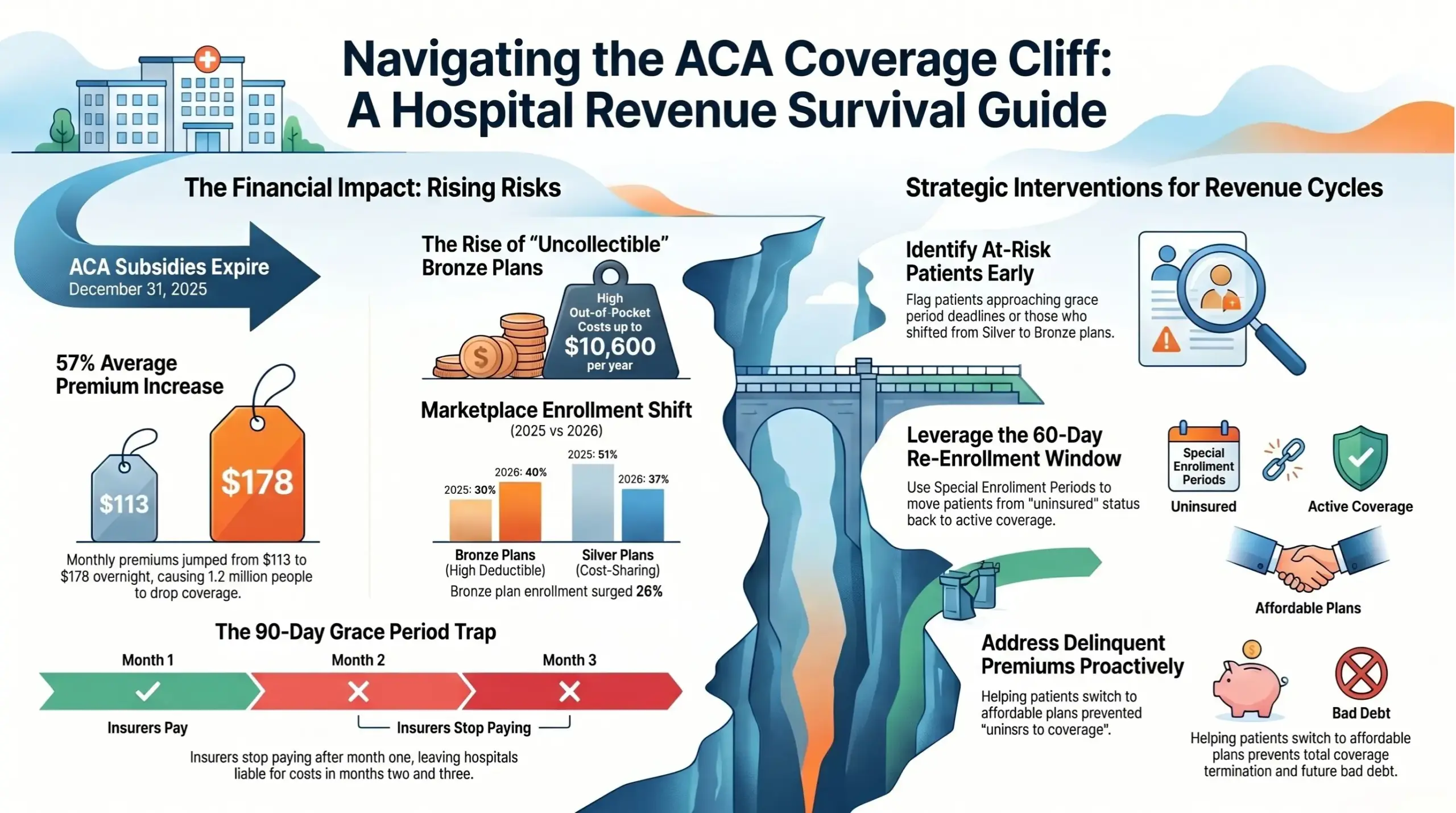

When Congress declined to renew the enhanced subsidies, average monthly marketplace premiums jumped from $113 to $178 overnight. National ACA Marketplace plan selections fell by about 1.2 million entering 2026, and large hospital operators are already reporting early signs of the impact in Q1 earnings calls. This is not a future problem. It is a present one hitting revenue cycles right now.

If your team is not actively responding to the coverage cliff, you are already behind.

What the Coverage Cliff Actually Means for Hospitals

Enhanced premium tax credits, first introduced in 2021 and extended through 2025, capped monthly premiums at 8.5 percent of household income. When they expired, households earning above 400 percent of the federal poverty level lost subsidies entirely, and lower-income households saw their credits shrink. The average nonsubsidized premium climbed to $746 per month, up from $612 the year before.

Many patients dropped coverage, downgraded to bare-minimum plans, or stopped paying their premiums altogether. The effects are already visible in hospital financials. HCA Healthcare reported a 15 percent year-over-year drop in marketplace equivalent admissions in Q1 2026 and a corresponding 16 percent increase in uninsured equivalent admissions. Universal Health Services absorbed an estimated $15 million pretax hit in Q1 alone, with its CFO warning the impact would grow larger as the year progresses. These examples may signal broader pressure ahead for health systems, especially those with meaningful Marketplace patient volume.

The Bronze Plan Shift and What It Means for Collections

Even patients who stayed enrolled have changed behavior in ways that affect collections. Bronze plan enrollment surged 26 percent nationally in 2026, rising from 30 percent to 40 percent of total ACA enrollment. Bronze plans carry the lowest premiums but the highest out-of-pocket costs, with a maximum cap of $10,600 per year. Patients on bronze plans are significantly harder to collect from than those on silver or gold plans.

At the same time, enrollment in cost-sharing reduction eligible silver plans dropped from 51 percent in 2025 to 37 percent in 2026. Fewer patients qualifying for cost-sharing reductions means more collection exposure at the point of care. If your financial planning models have not been recalibrated to reflect this shift, that gap deserves urgent attention.

The Grace Period Trap

Under ACA rules, patients receiving premium assistance who fall behind on premiums have a 90-day grace period before coverage terminates. The insurer is required to cover care only during the first month. The second and third months create a revenue risk: hospitals provide care under the assumption of coverage, claims are submitted and processed, and then recoupment occurs when coverage is retroactively terminated.

For patients who enrolled in 2026 plans and stopped paying after their first bill arrived, that recoupment cycle is moving through revenue cycle departments right now. Identifying those patients before they hit the termination point is the intervention that matters most. Once coverage terminates, recovery options narrow and the balance is much more likely to become self-pay, charity care, or bad debt.

How to Respond: Three Priorities

Identify at-risk patients before coverage lapses.

Flag marketplace patients approaching grace period deadlines, patients who have shifted from silver to bronze plans, and patients with income near the subsidy cliff. Proactive identification creates the window for intervention. Reactive identification after termination leaves far fewer options.

Accelerate re-enrollment for patients who have dropped coverage.

Loss of marketplace coverage is a Qualifying Life Event, which gives patients a 60-day special enrollment window. Most patients who drop coverage do not know this exists. Patient access and financial counseling teams that actively inform eligible patients of this option, and support them through enrollment, may be able to convert some uninsured encounters into insured ones.

Address delinquent premiums before they trigger termination.

Connecting at-risk patients with financial assistance resources, helping them switch to more affordable plans, or clarifying their subsidy eligibility all reduce the probability of termination and recoupment. Prevention costs substantially less than uncompensated care.

Looking Ahead: 2027 Will Add More Pressure

The Medicaid semi-annual redetermination requirement takes effect January 1, 2027. States will be required to redetermine eligibility for the expansion population every six months, and some analyses project that Medicaid expansion enrollment could fall by several million people as a result of new eligibility and redetermination requirements. For many of those patients, the ACA marketplace will be the alternative pathway. Hospitals that have already built enrollment infrastructure will be positioned to facilitate that transition. Those that have not will see Medicaid revenue replaced by uncompensated care.

Federal funding for marketplace enrollment navigators was sharply reduced in 2025, leaving dramatically fewer resources available to help patients enroll. The hospitals that fill that gap will recover revenue that would otherwise become bad debt.

Act Now, Before the Second Wave Hits

The ACA coverage cliff is a current financial reality, not a future risk. Marketplace enrollment is down, uninsured admissions are up, and collection challenges from high-deductible bronze plans are intensifying.

The revenue impact is not fixed. Patients who have lost coverage can be re-enrolled. Patients in the grace period can be identified before termination. Each of those interventions can help reduce the likelihood that otherwise reimbursable care becomes uncompensated. The teams that build this capability now will be better positioned when Medicaid redetermination pressure hits in 2027.

RevOne Companies has been partnering with hospital revenue cycle teams since 2003 to convert uninsured patients into insured ones. Our MyCareCoverage platform, Delinquent Premium Monitoring service, and community-based enrollment support teams are designed to help hospital revenue cycle teams respond to this type of coverage disruption.